Someone recently asked me when I’d release a new edition of Digitize or Die. My answer surprised even me: the book doesn’t need a new edition. The title says it all — and right now, it says it louder than ever. What has changed is the cost of not acting. It used to be measured in years of lost ground. Today it’s measured in quarters. A three-person team with the right AI stack can now replicate what took your engineering department five years to build — in eight weeks. The tool is available to everyone. The transformation is not.

This post focuses exclusively on pure SaaS companies — no hardware products involved (that’s a separate piece). The questions I want to work through: What is AI actually doing to software economics right now? What does it transform, what does it destroy, which skills does it make obsolete and which does it make more valuable than ever? And most importantly — what does a company need to do, concretely, to still be standing in five years?

1What is actually happening?

We are living through the fastest structural shift in software economics since the move to the cloud. The signals are everywhere and they are compounding.

Enterprise AI adoption has roughly doubled in two years: 78% of organisations now use AI in at least one business function, up from 55% in 2023. Corporate AI investment reached $252 billion globally in 2024, up 44.5% year-over-year. Gartner forecasts worldwide AI spending at $1.5 trillion in 2025. Meanwhile OpenAI’s frontier reasoning model dropped 80% in price in just two months — the cost curve of intelligence is accelerating downward even as capability improves.

Organisations using AI in at least one function in 2025, up from 55% in 2023

Source: McKinsey / FullView

Global corporate AI investment in 2024 — a 44.5% year-over-year increase

Source: FullView AI Statistics 2025

Share of all SaaS M&A transactions referencing AI in 2025, a 12× increase since 2018

Source: Software Equity Group

Of all code written in 2025 is now AI-generated or AI-assisted

Source: Index.dev / GitHub

Bain & Company summarises it well: “In three years, any routine, rules-based digital task could move from ‘human plus app’ to ‘AI agent plus API.'” That is not a prediction about some distant future — it is happening now, quarter by quarter.

“64% of SaaS CEOs believe generative AI is already lowering barriers to entry in their market.”

— Software Equity Group, AI in SaaS Survey Q4 2025 (n=450 SaaS CEOs)

2The impact on software creation

The most immediate and concrete consequence of this shift is a brutal compression of development costs and timelines. Software will be built faster and cheaper than at any point in history — and the gap is widening every month.

The speed numbers

Productivity gains reported by developers using AI coding tools

Sources: Sida Peng et al. (2023) arXiv:2302.06590; Index.dev 2026; TechReviewer 2025; Second Talent 2025; Netcorp Software Development

One striking example: a multi-company RCT across Microsoft, Accenture, and a Fortune 100 enterprise with nearly 5,000 developers found a 26% average productivity increase with GitHub Copilot — the equivalent of turning an 8-hour workday into 10 hours of output. The gains were especially pronounced for junior developers, who saw 35–39% speed-ups.

By 2026, 84% of developers use AI tools, and 41% of all code is AI-generated. GitHub Copilot alone has over 15 million users — a 4× increase in a single year — and is deployed at 90% of Fortune 100 companies.

A note of nuance: speed isn’t the whole story

The picture is more complex than pure gains. A 2025 METR study found that experienced developers working on complex open-source repositories actually took 19% longer with AI tools — a reminder that AI acceleration is task-dependent. Code churn is up 26% year-over-year. Duplication has increased 4×. Nearly 46% of developers don’t fully trust AI outputs and spend additional time reviewing.

The bottom line for software businesses: the cost of producing initial features is collapsing, but the cost and value of architecture, integration, security, and maintainability is rising. This distinction will prove decisive.

“AI is not a cost saver — it is a value accelerator. Companies that move early report $3.70 in value for every dollar invested, with top performers at $10.30.”

— FullView AI Statistics 2025, citing multiple primary studies

3What this creates, destroys, and transforms

The transformation of the Product Manager

The product manager’s job is about to change radically. For the last decade, PMs have spent enormous energy on one problem: translating customer needs into precise specifications, because development was expensive and slow. You had to get it right on paper before anyone touched a keyboard.

That constraint is dissolving. The new model looks something like this: a PM — equipped with a standardised context stack (think a CLAUDE.md file that defines the tech stack, UI templates, data models, and guardrails) — can now build a live POC directly with a customer, on their premises, within a few days. The spec emerges from the prototype, not the other way around. Communities can validate direction in weeks rather than quarters. The PM becomes a product engineer who speaks the customer’s language and AI’s language simultaneously.

This is not a small shift. It changes the nature of what we hire for, how we structure teams, and what “good product work” looks like.

The evolving role of developers

Developers won’t disappear — but their centre of gravity is moving. As AI handles an increasing share of feature-level code generation, the scarce and valuable work becomes:

- Architecture — designing systems that are scalable, composable, and secure from first principles

- Domain context — understanding the business deeply enough to know which AI output is actually correct

- Security and integrity — especially as 48% of AI-generated code contains potential vulnerabilities that need human review

- Integration — connecting AI-generated components into larger, production-grade systems

The developer who thrives in this era is less “someone who writes code” and more “someone who orchestrates code production and guarantees its fitness for a larger purpose.”

The disruption of Design — and the rise of UX

Design and UI specialists are facing a disruption just as profound as developers — perhaps more visible, because the signs are already everywhere. Tools like Figma’s AI features, Midjourney, and a growing wave of design-to-code platforms can now generate polished, consistent visual interfaces from a prompt in seconds. The barrier to producing a professional-looking UI has essentially collapsed.

This has a direct strategic consequence: UI as a competitive differentiator is disappearing. If any well-funded startup can ship a beautiful, pixel-perfect interface in days — and they can — then the fact that your product looks good is no longer a moat. It is table stakes, nothing more. The visual layer is being commoditised at the same pace as feature development.

“If your differentiation lives mostly in UI and automation, that’s no longer enough. The barrier to entry has dropped, which makes building a real moat much harder.”

— Igor Ryabenkiy, Managing Partner at AltaIR Capital, TechCrunch March 2026

But here is the twist: while the value of UI is compressing, the value of UX — genuine user experience design — is rising. These two disciplines are often conflated, but they are fundamentally different in the AI era.

UI Design

The visual and graphic layer — colour systems, typography, layout grids, component libraries, icon sets, motion effects. AI generates all of this fluently and at speed. The “look” of software is no longer a differentiator.

- Visual component production

- Design system tokens & theming

- Responsive layout generation

- Brand-to-code translation

UX Design

The strategic and human layer — understanding how users actually think and fail, designing flows that reduce cognitive load, embedding deep domain knowledge into interactions. AI cannot substitute for this because it requires human empathy and context.

- User research and behavioural insight

- Jobs-to-be-done mapping

- Cognitive load reduction & error design

- Domain-specific workflow orchestration

The UX designer of tomorrow is less a visual craftsperson and more a behavioural architect — someone who understands deeply what users are trying to accomplish, where they get lost, what they trust, and what makes them come back. That knowledge, rooted in customer intimacy and domain expertise, is precisely what AI cannot generate. It has to be earned through observation, iteration, and proximity to real users.

For software companies, the implication is clear: investing in surface-level UI polish is a diminishing return. Investing in UX research, in understanding the full job-to-be-done, in designing for the specific cognitive and emotional context of your vertical — that is where differentiation lives now.

Enterprise SaaS: the reckoning

Enterprise SaaS companies have suffered dramatically on equity markets — and the anxiety is rational. The historical moat of enterprise SaaS was built on three pillars: the capital required to hire a development team (several million minimum), the time required to reach product-market fit, and the customer acquisition cost and install base needed before profitability showed up (5,000 to 10,000+ seats). These barriers made competition nearly impossible for small players.

AI is systematically lowering all three barriers simultaneously. Markets that once supported a handful of dominant vendors are now seeing dozens of viable challengers built by small teams in weeks, not years.

Key disruption risk factors for SaaS categories

Sources: Gartner 2025; Forrester “SaaS as We Know It Is Dead” 2026; Software Equity Group Q4 2025; Stax Consulting “How AI Is Reshaping Vertical SaaS” 2026

A key structural divide is emerging, well captured by Stax Consulting: “The gap between mission-critical platforms and peripheral tools is widening.” AI may lower the cost of building tools at the edges, but maintaining a platform that stores authoritative data, enforces contracts, reconciles finances, and governs workflows is an ongoing operational commitment — one that vendors can amortise across thousands of customers but individual businesses cannot.

4My thesis: how companies can thrive

Customers’ demands are not shrinking — they are transforming. In a world where basic software becomes cheap, the premium goes to what cannot be easily replicated: deep vertical knowledge, proprietary data, reliability at scale, cybersecurity, and human trust networks.

Bain’s analysis is clear: “Your data is your moat. While models like GPT-4o are everywhere, the real value lies in the proprietary data you own.” A16z’s January 2025 report arrives at the same conclusion: as foundation model capabilities commoditise, scarcity shifts from the model to the data.

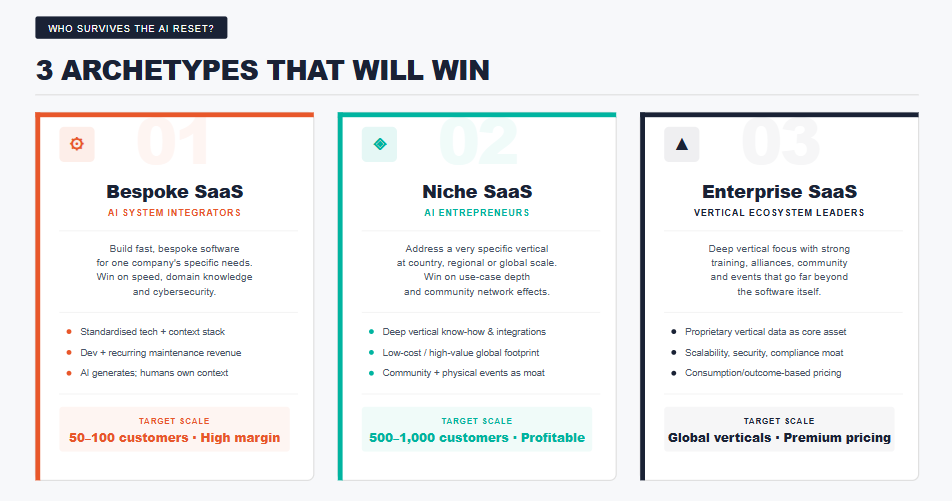

The three archetypes that will win

Bespoke SaaS

AI System Integrators

Build fast, bespoke software for specific company needs. Win on speed, deep customer use-case knowledge, and cybersecurity.

- Standardised technology and context stack (stack, UI templates, deployment)

- Revenue from development + recurring maintenance contracts

- Can serve 50–100 clients at very high margins

- AI agents do the heavy lifting; humans handle customer context

Niche SaaS

AI Entrepreneurs

Address a very specific vertical niche at country, regional, or global scale. Win on use-case depth and community.

- Deep know-how in integrations, processes, and regulations that would take years to replicate

- Low-cost / high-value software with global footprint potential

- Community layer — physical events, peer knowledge exchange — as a powerful retention moat

- Network effects from shared proprietary data

Enterprise SaaS

Vertical Ecosystem Leaders

Deep vertical focus with strong training, alliances, community, and event ecosystems that go far beyond the software itself.

- Proprietary industry data as the core competitive asset

- Strong compliance, scalability, and cybersecurity positioning

- Shift from per-seat to consumption / outcome-based pricing

- Ecosystem lock-in: certifications, partner networks, events

What will be commoditised — and what won’t

| Capability | AI Disruption Risk | Rationale |

|---|---|---|

| Feature development (standard CRUD, workflows) | Very high | AI generates this in seconds. Barriers are near zero. |

| UI/UX differentiation (interface only) | High | Investors explicitly say “UI differentiation is no longer enough.” |

| Horizontal SaaS without data moat | High | Point solutions being replaced by AI agents. Seat-based pricing under pressure. |

| Proprietary vertical data | Very low | Becomes more valuable as models commoditise. The scarce input every agent needs. |

| Community, training, physical events | Very low | Human trust networks cannot be replicated by AI. Major retention moat. |

| Mission-critical / regulated software (SCADA, healthcare, industrial) | Low | High switching cost, compliance requirements, safety scrutiny insulate incumbents. |

| Systems of record (ERP, CRM, financial ledgers) | Medium | Core data remains essential; but per-seat model is under pressure from agent efficiency. |

| Cybersecurity & compliance positioning | Very low | Enterprises pay premiums for auditability. “CrowdStrike proves security = pricing power.” |

“LLMs are systematically dismantling the moats that made vertical software defensible. But not all of them.”

— Nicolas Bustamante, founder of Doctrine and Fintool, cited in Medium / Rob Saker, Feb 2026

A word on the companies that will struggle most

The most exposed category is pure SaaS companies whose only differentiation is a large codebase and a feature set. These are companies that never built a data asset, a community, a certification ecosystem, or a compliance moat. They raised capital to build features; AI now replicates those features in days. Forrester put it bluntly in early 2026: “SaaS as we know it is dead.” That’s an overstatement — but the underlying point is real: the historical barriers are gone, and companies without a new basis for differentiation are exposed.

Multiple SaaS companies reported slowing growth in Q4 2025 earnings — not because AI failed to deliver productivity, but precisely because it did. Customers are reducing software seats as AI-enhanced workers accomplish more with fewer licences.

What survives and why

Vertical SaaS with proprietary data, mission-critical workflows, and community will not only survive — it will grow. The vertical software market is projected to expand from ~$134B in 2025 to $194B by 2029. The companies that understood their core product was the knowledge, trust, and data inside the software — not the software itself — will emerge from this reset stronger.

The companies that thought their moat was their codebase? They need to move. Fast.

Digitize or Die — the thesis holds. The urgency just multiplied.

When I first wrote Digitize or Die, the central argument was this: companies that refused to embrace digital transformation wouldn’t be killed by technology — they’d be killed by the distance that opened up between them and the companies that did embrace it. Competitors who moved faster, served customers better, operated leaner. The threat was never the tool. It was the decision — or the paralysis.

AI doesn’t change that thesis. It accelerates it to an almost uncomfortable degree.

AI is not what kills companies. What kills companies is choosing not to transform — or transforming too slowly while others don’t hesitate.

The companies that will disappear in the next five years won’t be victims of AI. They’ll be victims of their own inertia. They’ll be companies that watched the transformation coming, debated it in committees, ran a pilot or two, and woke up one morning to discover that a three-person team had shipped a credible alternative to their core product in eight weeks — for a fraction of the price, with a better UX, trained on their own customers’ data.

The uncomfortable truth is that AI makes transformation both more urgent and more accessible than ever before. The barrier to acting has never been lower. The cost of not acting has never been higher. There is no longer a credible excuse rooted in budget, in team size, or in technical complexity. A motivated team with the right domain knowledge and the right AI tools can now move faster than a 200-person engineering department that hasn’t adapted its ways of working.

This is the part that no technology can fix for you. AI can generate your code, your designs, your specifications, your documentation. It cannot generate the leadership decision to change, the organisational courage to cannibalise a business model before a competitor does, or the customer intimacy that tells you which transformation actually matters.

Those who thrive will be the ones who treat AI not as a threat to manage but as leverage — leverage to go deeper into their vertical, to serve fewer customers far better, to build the kind of trust and knowledge compound that no model can replicate from the outside. The tool is available to everyone. The transformation is not.

↗The bottom line

The era of raising $5M to recruit a development team and build a defensible feature set is over. In its place, three things matter:

- Data propriety: Do you own data your customers can’t get anywhere else?

- Ecosystem depth: Do customers buy your knowledge, community, and trust — not just your software?

- Technical foundation: Is your architecture scalable, secure, and composable — ready for an AI-first world?

The good news for well-positioned companies: AI lowers the cost of building but raises the value of everything that can’t be built cheaply. Deep domain knowledge, proprietary data, and human community are harder to replicate than ever — because any well-funded competitor can now generate the feature set you spent five years building, in six weeks.

Next post: the same questions for SaaS + hardware companies — where the picture is very different.

Sources & References

- FullView.io — “200+ AI Statistics & Trends for 2025” fullview.io/blog/ai-statistics

- Bain & Company — “Will Agentic AI Disrupt SaaS?” Technology Report 2025 bain.com

- Bain & Company — “Why SaaS Stocks Have Dropped” 2026 bain.com

- Software Equity Group — “The AI Reset: How SaaS Founders Can Reinvent” Q4 2025 softwareequity.com

- Forrester — “SaaS As We Know It Is Dead” 2026 forrester.com

- Stax Consulting — “How AI Is Reshaping Vertical SaaS” 2026 stax.com

- TechReviewer — “AI in Software Development 2025: From Exploration to Accountability” techreviewer.co

- TechCrunch — “Investors spill what they aren’t looking for anymore in AI SaaS” March 2026 techcrunch.com

- Sida Peng et al. — “The Impact of AI on Developer Productivity: Evidence from GitHub Copilot” arXiv 2302.06590 (2023) arxiv.org

- METR — “Measuring the Impact of Early-2025 AI on Experienced Open-Source Developer Productivity” July 2025 metr.org

- DORA 2024/2025 Reports — Google Cloud / Axify axify.io

- Index.dev — “Top 100 Developer Productivity Statistics with AI Tools 2026” index.dev

- Second Talent — “GitHub Copilot Statistics & Adoption Trends 2025” secondtalent.com

- SaaStr — “The Great B2B Bifurcation of 2025” Dec 2025 saastr.com

- Medium / Rob Saker — “AI Is Eating Enterprise SaaS” Feb 2026 medium.com